The digital payments boom seen in recent years brought with it the emergence of new ways of understanding the world of payments, which go beyond the traditional financial institutions. This shift was led by new players, fintech companies, which broke into the banking industry with new and innovative technologies designed to improve and automate the financial services and transactional processes of other organizations, companies, and individuals in the ecosystem.

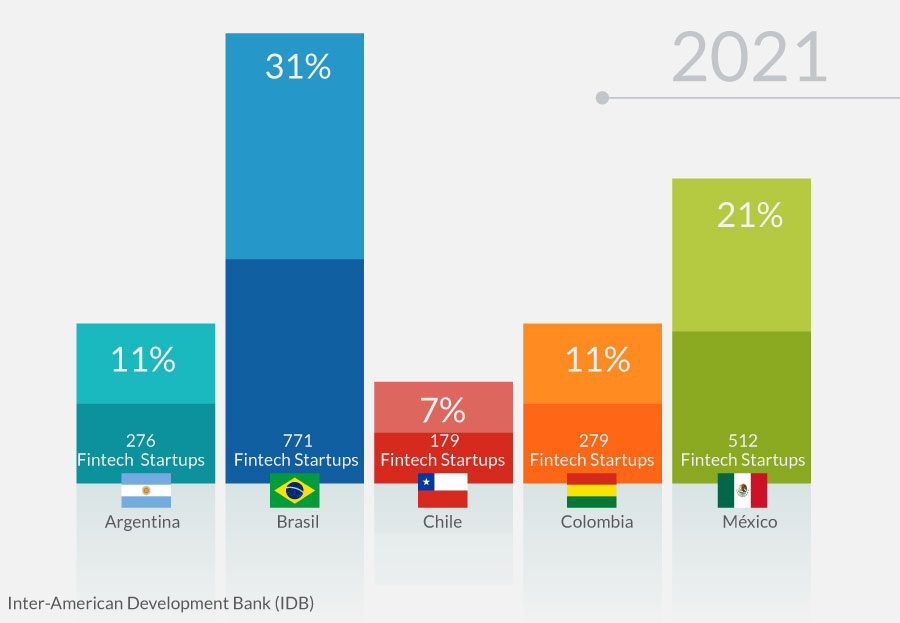

According to a study conducted by the Inter-American Development Bank (IDB) and Finnovista, the fintech ecosystem grew by 112%, from the time these organizations conducted the same analysis in 2018 —with a total of 1,166 startups— and in 2021 —with a total of 2,482 startups.

Currently, there are five Latin American countries that show the highest growth rates in this field, representing 81% of all fintech companies in the region. Among them is Chile, which contributes 179 startups to this count.

On average, the total number of startups in this group of countries has grown at a yearly rate of 34% between 2017 and 2021. In Chile’s case, the growth rate has been 175% for the same period.

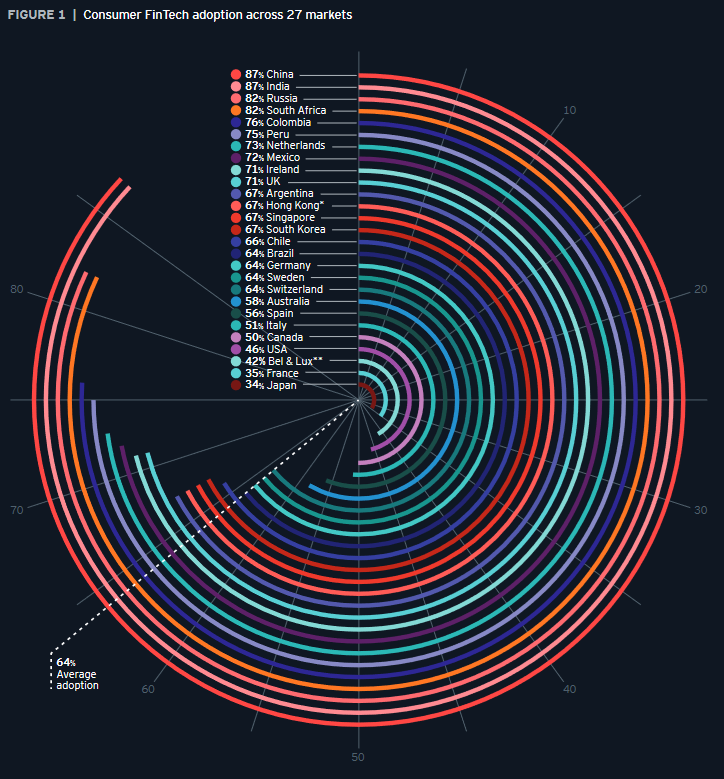

These numbers show fintech adopters as a percentage of the digitally active population in each market.

Evidence of the remarkable moment that fintechs are currently experiencing in Chile is that, in 2021, they attracted an investment of almost $3 billion in venture capital. Some of the factors that helped boost the innovation ecosystem in the country —home to the “unicorns” Betterfly and NotCo— were: 1) the support given by the public administration and state-sponsored accelerator, Start-Up Chile; 2) the access local entrepreneurs have to foreign markets; and 3) the variety of startups, ranging from sectors like agrotech to innovations in mining, and the large presence of fintechs in the local market.

Introduction to the Regulatory Framework

The new Fintech Law, enacted on October 12, 2022, became a turning point in terms of local regulation. This law reforms the marketing of crowdfunding platforms, alternative transaction systems, credit and investment consulting services, custody arrangements of financial instruments, and the routing of orders and brokerage of financial instruments.

Under the new law, it will be required to demonstrate capabilities in operational matters, transparency in disclosing potential conflicts of interest, expertise in consulting, guarantees, and minimum levels of assets available to be able to respond to clients in case any problems arise.

Regulatory Scope and Requirements

| Description | Crowfunding platform | Alternative transactional systems | Financial institutions intermediaries | Orders routing | Financial/credit advisors | Custodians |

|---|---|---|---|---|---|---|

|

Information and registration |

|

|

|

|

|

|

|

System and people suitability |

|

|

|

|

|

|

|

Corporate governance and risk management |

|

|

|

|

|

|

|

Operational capacity |

|

|

|

|

|

|

|

Guarantee |

|

|

|

|

|

|

|

Heritage |

|

|

|

|

|

|

Currently, Evertec is among the top 100 fintechs in the region, bringing countless disruptive technologies to the market that provide value-added to their customers and comply with current market regulations. Digital acceleration has positioned Evertec as a partner for clients and entities that find value in leveraging the technological evolution to improve the experience of users and customers.

By José Luis Godoy

José Luis Godoy

Gerente de Tecnología

Profesional con más de 22 años en la industria tecnológica y amplia experiencia liderando equipos de TI en áreas como Infraestructura, Producción, Administración de Datos, Programación y Soporte. Actualmente, Gerente de Tecnología en Evertec Chile.